While doing payroll processing for your clients, expect to get bombarded with questions like “One employee’s net pay looks wrong. Can you check before Monday?” and “HMRC says our FPS was late, are we getting a penalty?” It shows that payroll processing is not as simple as it sounds.

When you start with payroll processing, you will have to deal with deadlines, RTI submissions, pension uploads, holiday pay queries, and many more. No wonder it is high-risk, high-pressure, but an important responsibility for your practice. Any mistakes here will lead to inaccurate or delayed payments, breaking the trust of the employees and of your clients in you.

To help you streamline your payroll processing, we have created this guide. Here we have broken down the payroll process, the compliance rules that matter, the mistakes practices commonly make, and most importantly, why outsourcing payroll processing services is becoming a strategic decision for UK practices in 2026.

Let’s dive into the world of payroll processing.

What Is Payroll Processing and Why Does It Matter for UK Firms?

Payroll processing involves calculating employee salaries, deductions and taxes, as well as ensuring that payments are made correctly and on time. The responsibility of handling this was with respective companies’ HR and payroll departments, but now accounting practices are handling the process and keeping it compliant as per payroll regulations on their behalf.

Payroll processing includes:

- Calculating gross pay

- Applying PAYE income tax and National Insurance

- Handling statutory payments (SSP, SMP, etc.)

- Submitting RTI returns

- Paying employees correctly and on time

Why it matters so much in the UK:

- Payroll errors directly affect your client employees’ take-home pay

- Payroll errors UK will lead to HMRC applying penalties quickly

- One mistake can cost you the trust of your client

A survey conducted by Access Paycircle as part of PeopleHR’s UK Payslip Anxiety Report shows that 63.85% employees claimed to have received incorrect pay during their employment. This statistic will add pressure to your small accounting practice.

What Are the Key Steps Involved in Payroll Processing?

The strength of a payroll process depends on clear steps. These steps are:

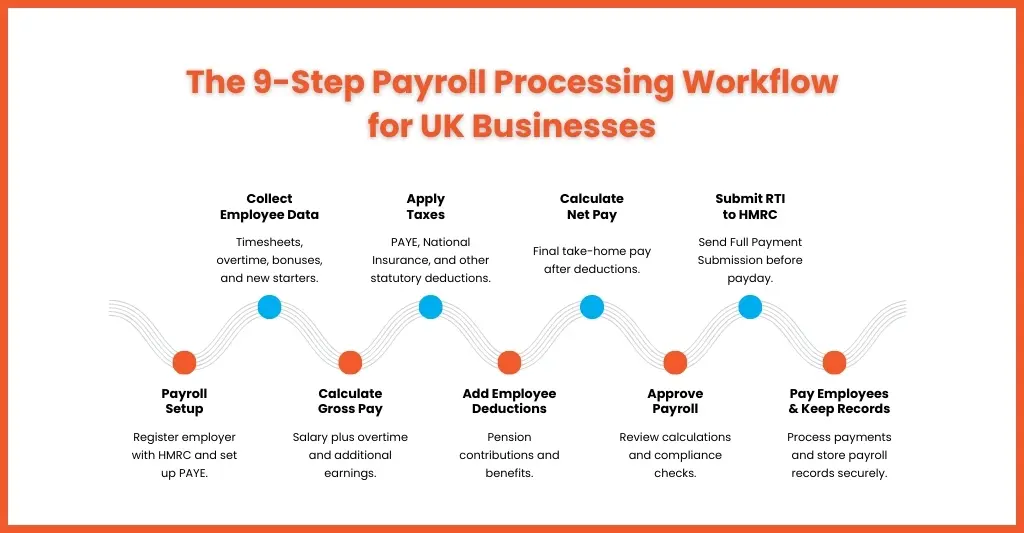

Complete All Payroll Setup Tasks

Before starting the payroll processing for your client, ensure that the initial setup is carried out. It includes registering your client with the HMRC as an employer and setting up a PAYE Online account, as well as making your client understand its legal obligations.

Understanding legal obligations is important because it ensures your client stays compliant with HMRC regulations or else faces penalties.

Calculate Gross Pay

Once you have set up the PAYE account for your client and chosen the software, you must start calculating the gross pay for each of their employee. This is done by multiplying their pay rate by the number of hours worked within the pay period to get their base salary.

Also include any overtime pay, bonuses or additional earnings to calculate their gross pay. Not including these additional earnings will lead to incorrect deductions and tax calculations, so take care of that.

Calculate Payroll Taxes

It is important to calculate payroll taxes to ensure that your clients’ compliance and the employees are paid accurately. Any mistakes in this could spoil the relations between the employee and your employer client or lead to legal consequences for your clients and bad repute for you.

The tax each employee has to pay will depend on their tax code and National Insurance. Use the calculators offered by HMRC to check calculations for payroll like tax, National Insurance contributions, and student loan deductions.

Determine Employee Deductions

Identify any other deductions such as pension contributions, health insurance premiums, and other benefits. Understand the importance of differentiating between pre-tax deductions and post-tax deductions and ensure it is calculated at the right point of the payroll process for accurate payments.

Calculate Net Pay

Once the taxes and employee deductions are calculated, you need to deduct them from the gross pay. The amount left is called the net pay, also called the final amount, which the employee takes home.

Approve Payroll

Conduct a thorough review of the processing to make sure that each employee is paid correctly and that it is in compliance with the latest HMRC payroll regulations. It might be tempting to skip this step, especially during busy periods, but it’s an important safeguard against payroll errors and discrepancies.

Payment to Employees

Ensure the payroll is processed on time to maintain employee trust. These payments can be made via BACS, online payment, cheque or cash. Also, make the payslip available to the employee, and it must show their earnings before and after deductions.

File Tax Reports on Time

After processing and paying the employees, make sure all the payroll tax reports and deductions are passed on to the HMRC. Keep tabs on the legislation associated with it to remain compliant with the latest changes.

Maintain Accurate Records

The final step of payroll processing is maintaining the records and keeping them secure in a digital format in an encrypted cloud storage. These records must be compliant with the latest MTD for payroll regulations.

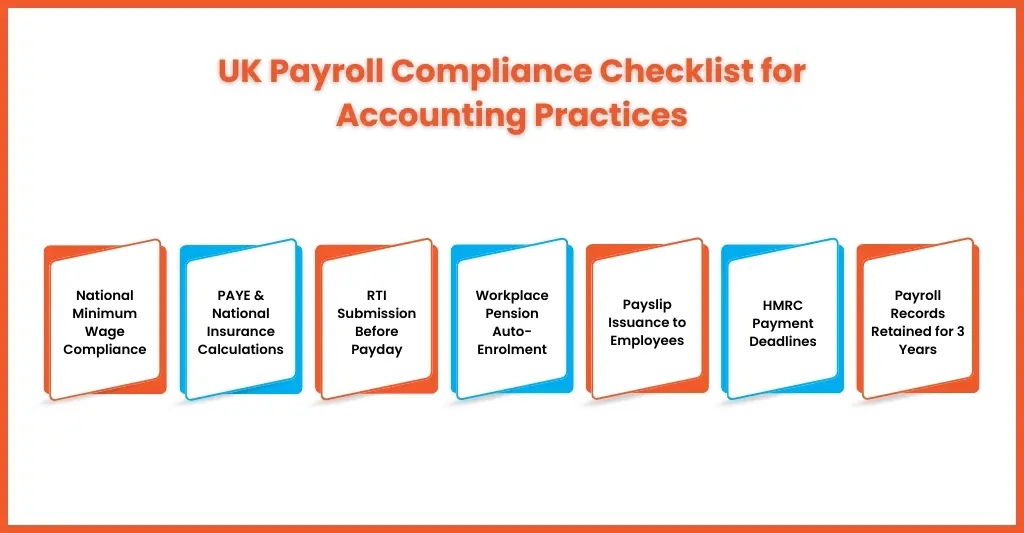

Payroll Processing Compliance in the UK — What Every Employer Must Know

UK payroll is heavily regulated, which makes payroll compliance a necessity. Here are some key payroll compliances you will need to follow:

National Minimum Wage (NMW) and National Living Wage (NLW)

The National Minimum Wage and National Living Wage are applicable to employees depending on their ages. Track work time and attendance to apply the correct wages in accordance with the law.

Pay As You Earn (PAYE)

PAYE is HMRC’s system for collecting Income Tax and National Insurance Contributions (NICs) from employment.

National Insurance Contributions (NICs)

Your client needs to pay NICs on their employees’ earnings. The rates will depend on the earnings. Most of your client employees will come under Class 1 NICs.

According to HMRC, an employee’s Class 1 National Insurance is made up of contributions:

- Deducted from their pay (employee’s National Insurance)

- Paid by their employer (employer’s National Insurance)

- Real Time Information (RTI)

As per RTI, all payroll data must be submitted in real time to HMRC. Late submissions will trigger automatic penalties.

Workplace Pensions

Auto-enrolment compliance under The Pensions Regulator is mandatory. Missed contributions can lead to fines.

Keep Records

All payroll records must be stored for 3 years from the end of the tax year. HMRC might demand the records for audit purposes.

Common Payroll Processing Mistakes UK Practices Make (and How to Avoid Them)

As an experienced accounting practice, you might treat payroll processing as routine until something goes wrong. Let’s understand some of those common mistakes made in payroll processing and how they can be avoided.

Late RTI Submissions

Under Real Time Information rules, the Full Payment Submissions must be sent to the HMRC on or before the pay day. Missing it will lead to penalties.

Late RTI submissions usually happen because:

- Clients send overtime or bonus data late

- Amendments are made after payroll is processed

- No formal cut-off time exists

- One staff member handles all payroll and is unavailable

- Late submissions at regular intervals will damage your practice reputation.

How to avoid it:

- Set strict payroll cut-off dates and communicate them clearly

- Create a standard payroll calendar for all clients

- Process payroll at least 2–3 working days before the pay date

- Build buffer time for amendments

Incorrect Tax Codes

Adding incorrect tax codes is one of the quickest ways to demoralise an employee. Such an error leads to:

- Overpaid or underpaid tax

- Employee complaints

- Year-end reconciliation headaches

Tax codes change through:

- P6 notices

- P9 notices

- Emergency code updates

- Starter checklist submissions

When these notices are ignored, an error occurs.

How to avoid it:

- Review HMRC notifications weekly

- Assign a dedicated accountant for monitoring tax code updates

- Cross-check codes during each payroll run

Accurate tax coding protects both your client and your reputation.

Pension Errors

Auto-enrolment of a new employee under the pension regulator is compulsory.

Some of the common pension errors that occur are:

- Failing to enrol eligible employees

- Incorrect contribution percentages

- Missing re-enrolment dates

- Not processing opt-outs correctly

- Late pension submissions

Mistakes in pensions will attract heavy penalties from the regulator.

To avoid it, you will need to:

- Use payroll software with built-in pension checks

- Maintain a pension staging and re-enrolment calendar

- Reconcile pension deductions before submission

- Confirm contribution uploads after each payroll

Pensions are compliance-heavy, and a small mistake will cost your client dearly.

Holiday Pay Miscalculations

The frequency of holiday pay errors is rising in recent years, especially among:

- Variable-hours workers

- Overtime-heavy roles

- Shift-based employees

It has often been found that practices use outdated calculation methods, incorrect reference periods, and forget about regular overtime, which leads to this error.

How to avoid it:

- Use the correct 52-week reference period rules

- Include regular overtime where applicable

- Review holiday pay logic annually

- Ensure payroll software settings are updated

Payroll Journals Not Reconciled

It’s a problem that most practices overlook. Most focus on payroll processing, issuing of payslips, and transferring deductions to the HMRC. But the payroll journal isn’t properly reconciled in the accounts.

This creates:

- Management account mismatches

- Incorrect expense reporting

- Year-end adjustments

- Frustrated auditors

Often, payroll journals are posted automatically but never reviewed.

To avoid it, you will need to:

- Reconcile payroll control accounts monthly

- Match PAYE liability accounts to HMRC payments

- Review pension creditor balances

- Do payroll reconciliation in your monthly close checklist

In-House vs Outsourced Payroll Processing — Which Is Right for Your Practice?

In-House Payroll

Pros:

- Direct control

- Familiarity with clients

Cons:

- Staff dependency

- Peak-period stress

- High compliance risk

- Limited scalability

Outsourced Payroll Processing

Pros:

- Specialist focus

- Reduced risk

- Scalable capacity

- Consistent service levels

Cons:

- Requires structured handover

- Needs clear communication

Due to complex payroll regulations in the UK, payroll processing has become time-consuming and generates less revenue. In the in-house vs payroll outsourcing, practices are finding it beneficial to avail themselves of the payroll outsourcing UK services.

Why Outsource Payroll Processing Services in the UK?

Outsourcing payroll is no longer an option for many small accounting practices; it has become a necessity and a tool to stay relevant when it comes to handling payroll processing, complex regulations, and staff shortages.

Yes, payroll outsourcing cost less compared to in-house payroll but practices are increasingly depending on outsourcing payroll because:

- It reduces payroll compliance risk

- Handle peak periods without hiring

- Eliminates dependency on one staff member

- Improves turnaround times

- Free’s senior staff for advisory work

Outsourcing will help you to maintain and improve your relations with your clients by fulfilling their payroll needs without falling into operational strain. Consider certain factors before you choose a payroll outsourcing partner, based on that you will find the best one for yourself.

How to Choose the Right Payroll Processing Software for UK Businesses

When you are looking for the right payroll software, look for the following features:

- HMRC-recognised RTI filing

- Automatic tax and NIC updates

- Pension integration

- Error alerts and validations

- Clear audit trails

Popular UK payroll platforms like Sage, BrightPay, and Xero Payroll have these features. You can choose the one that meets your requirements.

People Also Ask

How long does payroll processing take?

For a well-run payroll, processing typically takes a few hours per cycle. Complexity increases with variable pay, pensions, and multiple pay frequencies.

How much does outsourcing payroll processing services cost in the UK?

Costs vary based on employee numbers and complexity, but outsourcing is often more cost-effective than maintaining in-house payroll staff.

What happens if you make a payroll processing error in the UK?

Errors can lead to HMRC penalties, employee dissatisfaction, and reputational damage. Correcting errors often takes more time than doing payroll right the first time.

What are the 5 basic steps in processing payroll?

The 5 basic steps in payroll processing involve collecting employee data, calculating gross pay, applying deductions, processing payments, and maintaining records & compliance.

Which payroll software is best in the UK?

Popular UK payroll platforms like Sage, BrightPay, and Xero Payroll can be considered among ideal payroll software. However, the best software for you will be the one that meets your requirement and comes within your budget.

Conclusion

Here’s a reality check for all small accounting practices: payroll processing is going to get tougher this year, with many rule changes, tight deadlines, and high client expectations. All this will lead to high time consumption and limited value addition.

Such a situation will force you to:

- Keep the firefighting payroll every month

- Or build a payroll model that is accurate, compliant, and scalable

The smartest practices don’t remove payroll as a service.

It’s time to turn payroll from a source of stress to a source of benefit, and the first step towards that is by availing the payroll outsourcing services to get the job done. Equallto will make the transition smoothly and turn your payroll process into a profitable venture.

Time to act! Connect with us and get more details about our services. Looking forward to seeing you soon.