Payroll compliance is the process of ensuring the payroll is accurate, timely, and follows the UK employment, payroll and tax laws. For accounting practices, following payroll compliance is not a requirement; it’s a critical obligation that will help your clients and your reputation.

Let’s understand its importance through an example.

A small accounting practice in the UK had freshly onboarded multiple new clients. Things looked good until an HMRC inspection uncovered multiple problems, like:

- Late PAYE submissions

- Incorrect National Insurance calculations

- Missing pension contributions

These issues made their clients liable for fines, backdated payments, and frantic corrections.

The issue is not the capability of the practice but the lack of structured payroll compliance processes.

This story is not uncommon. According to HMRC, in 2026 multiple businesses faced fines payroll errors like underpaying below National Minimum Wage. Reports show that even minor errors in payroll processing can create administrative chaos, client dissatisfaction, and reputational damage.

It’s a story all across practices in the UK, creating administrative chaos, client dissatisfaction, and reputational damage. However, it can be avoided.

In this comprehensive guide, we’ll break down everything you need to know about payroll compliance, including:

- What payroll compliance is

- Why it matters

- Key components in the UK

- Common mistakes

- How technology can help

- And a full checklist for 2026

Key Takeaways

- Payroll compliance maintains accuracy in employee payments, statutory deductions, and adherence to UK laws.

- Non-compliance will lead to penalties for clients and reputational damage of your practice.

- All practices in the UK are required to comply with PAYE, National Insurance, pensions, and HMRC reporting.

- Organised workflows, periodic audits, and technology can reduce errors and save time.

- Outsourcing payroll to a trusted outsourcing partner like Equallto can help practices stay compliant and scale efficiently.

What Is Payroll Compliance?

Payroll compliance is the process of ensuring your payroll operations fully meet the UK legal, tax, and reporting obligations. When it comes to following payroll compliance in the UK, it means following the payroll legislation laid down by HMRC, including requirements for wage payments and tax deductions.

Under payroll compliance comes:

- Correct calculation of salaries, bonuses, and overtime

- Right deductions for PAYE, national insurance, pensions, and student loans

- On-time submission of payroll reports to HMRC via real-time information (RTI)

- Keeping up with changing tax legislation and employment laws

Why Payroll Compliance Matters for Your Practice

It’s important to maintain payroll compliance to shield your clients and yourself from surprise HMRC investigations, audits, and penalties. Through compliance, you will be able to:

Protect Clients and Employees

Compliance with payroll regulations will ensure that your client’s employees get their accurate pay, benefits, and statutory entitlement, thus avoiding disputes, legal hassle, and penalties.

Maintain Regulatory Compliance

These days HMRC and the pension regulator are enforcing regulation without compromise. Any loose ends with regards to payroll compliance will trigger an investigation and worst penalties.

Enhance Reputation and Trust

Payroll responsibilities are complex and time-consuming, which is why many businesses have entrusted these responsibilities to professional and experienced practices. Non-compliance from your end will lead to them paying fines and you losing the trust, reputation and business.

Reduce Resources Wastage

Non-compliance with HMRC payroll regulations will lead to payroll errors that must be resolved, leading to diversion of resources towards rework and client frustrations. Therefore, focus on compliance and save resources and time.

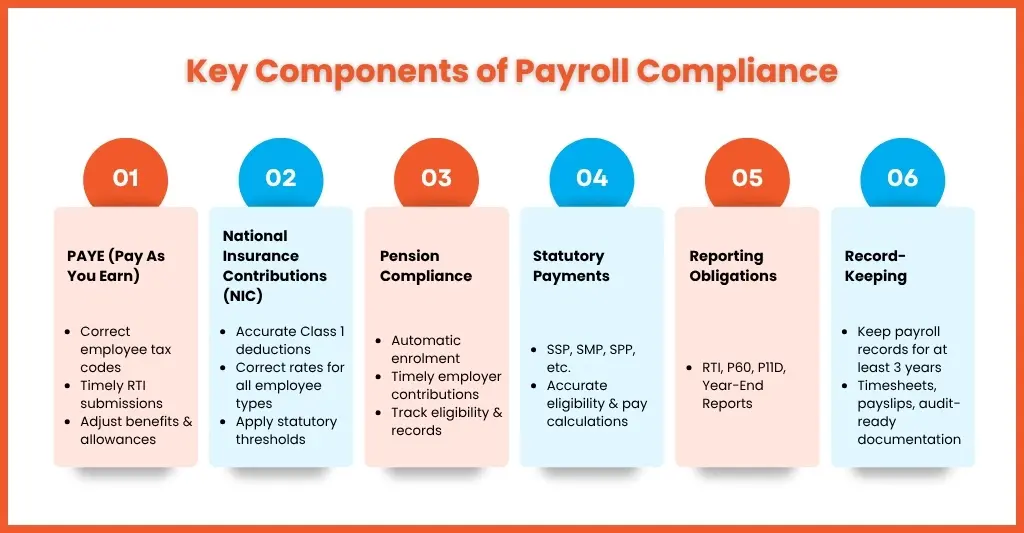

Key Components of Payroll Compliance in the UK

Payroll compliance in the UK has multiple aspects, and all of them must be given due attention. Let’s break down each element in detail.

PAYE (Pay As You Earn)

PAYE is a system in which employers can deduct income tax and national insurance contributions from their employees’ pay and submit it to HMRC.

What your practice needs to do:

- Correctly calculate employee income tax: Make sure all the employees of your client have applied for the right tax code, especially the newcomers.

- Timely RTI Submissions: All the payroll data of the employee must be submitted to HMRC in Real Time Information format on or before each payday.

- Adjust for benefits and allowances: Identify benefits given by your clients to their employee like car benefits, bonuses, and other taxable perks to ensure accurate deductions.

Delayed or inaccurate PAYE submissions are the most common cause of HMRC penalties and can trigger audits.

National Insurance Contributions (NIC)

National Insurance Contributions (NIC) are a UK tax on earnings paid by employees, employers, and the self-employed to fund state benefits, most notably the State Pension.

Compliance requirements:

- Accurate Deductions: Calculate Class 1 contributions for employees accurately and remit employer contributions on time.

- Adhere to Thresholds and Rates: Ensure you apply the correct rates for different employee categories, including under-21s, apprentices, and those on higher earnings.

- Adjust for Statutory Changes: NIC rates keep changing annually, so stay updated.

The ideal way to maintain compliance with NIC is by using payroll software like Xero, QuickBooks, and Sage and automating the calculation and submission process. Thereby reducing the risk of HMRC fines.

Pension Compliance

Since 2012, all employers have been required to comply with automatic pension requirements.

What you need to monitor:

- Automatic Enrolment: Make sure all eligible employees are automatically enrolled into workplace pensions.

- Timely Employer Contributions: Also, ensuring your clients’ contributions into the pension scheme are made on time to avoid penalties.

- Maintain Accurate Records: Keep a track of the number of clients’ employees coming in, going out, and contribution percentages for auditing purposes.

The Pensions Regulator can impose fines for missed contributions or failure to enrol eligible staff automatically.

Statutory Payments

Your employer clients are legally required to provide statutory pay when certain events happen.

These statutory payments are:

- Statutory Sick Pay (SSP): Paid to eligible employees who are off sick.

- Statutory Maternity, Paternity, Adoption, and Shared Parental Pay: These payments are based on an accurate calculation of employee eligibility and pay history.

- Accurate Calculations and Reporting: Incorrect calculations can trigger HMRC compliance checks and employee disputes.

Maintaining a clear system to track eligibility, duration, and rates ensures statutory payments are always compliant and avoids overpayment or underpayment errors.

Reporting Obligations

Payroll compliance is based on accurate reporting.

To do that, you will need to do:

- Real Time Information (RTI) Submissions: Each of your client is required to report pay and deductions after every payroll period.

- P60 forms: Issued annually to employees summarising total pay and deductions.

- P11D forms: Report taxable benefits and expenses for employees.

- Year-end reporting: Ensure all submissions are reconciled and filed by HMRC deadlines.

Use cloud payroll software to automate RTI submissions, generate P60s and P11Ds, and reduce human error.

Record-Keeping

Keep and maintain proper records because it’s a legal requirement.

What needs to be stored:

- Payroll records for at least three years that include pay, tax, and NIC calculations.

- Payslips of all employees

- Timesheets and payment histories are needed for audits and resolving employee disputes.

Maintaining accurate records protects your practice during HMRC inspections or employee queries. They also make HMRC’s audits and compliance checks faster and simpler.

The Ultimate Payroll Compliance Checklist

A payroll compliance checklist is not just a list of tasks; it’s your first line of defence against payroll errors, HMRC wage raid payroll check, penalties, and client dissatisfaction.

Here’s a practical checklist for 2026:

- Verify employee details that include name, National Insurance number, and tax codes

- Check salaries, overtime, and bonuses for accuracy

- Ensure correct deductions: PAYE, NI, pensions

- Submit RTI on time for each payroll cycle

- Generate payslips for all employees, ideally using cloud payroll software

- Maintain records for the statutory retention period

- Keep track of legislative changes, especially on changes in tax thresholds, NI rates, and MTD.

- Conduct an audit of payroll monthly to catch payroll errors before HMRC does

- Train your staff and the payroll teams of your clients on the latest compliance requirements.

- Explore payroll outsourcing support for expertise in payroll compliance

Common Payroll Compliance Mistakes and How to Avoid Them

Mistakes happen during practices while handling payroll compliance, but the cost of making these mistakes is costly and paid by your clients; it must be avoided at all costs. Let’s see some of the common mistakes:

Late RTI Submissions

As per UK payroll rules, Real Time Information (RTI) must be submitted to HMRC on or before payday. But many accounting practices miss it.

Why does this happen?

- Last-minute payroll processing

- Incomplete client data

- Manual workflows are causing delays

Impact of this mistake is:

- Automatic HMRC penalties

- Increased scrutiny from HMRC

- Potential compliance investigations

How to avoid it:

- Schedule payroll processing 2–3 days before payday

- Set automated reminders within your payroll system

- Maintain a checklist for each payroll cycle

- Ensure client data is collected in advance

Incorrect Tax Codes

Tax codes determine how much tax must be deducted, and a small mistake in this will cause serious trouble with the HMRC.

Why does this happen?

- Failure to update HMRC notices

- Incorrect setup for new employees

- Reliance on outdated data

Impact:

- Overpayment or underpayment of tax

- Employee dissatisfaction

- HMRC corrections and penalties

How to avoid it:

- Regularly check HMRC notifications

- Update tax codes immediately when changes occur

- Use payroll software that syncs with HMRC systems

- Double-check new employee setups

Missing Pension Contributions

Auto-enrolment for pensions is compulsory, but it often gets ignored.

Why does this happen?

- Missed contribution deadlines

- Incorrect employee eligibility tracking

- Lack of coordination between payroll and pension providers

Impact:

- Penalties from The Pensions Regulator

- Reputational damage to your practice

- Client’s employee dissatisfaction

How to avoid it:

- Maintain a clear schedule of pension deadlines

- Automate contribution calculations and payments using cloud payroll software

- Monitor employee eligibility regularly

- Reconcile payroll with pension reports

Inaccurate Statutory Pay Calculations

Statutory payments like SSP, SMP, and SPP require accurate calculations.

Mistakes happen in statutory pay calculations due to:

- Misunderstanding eligibility rules

- Incorrect calculation periods

- Manual calculation errors

Impact:

- Underpayment or overpayment

- Compliance issues with HMRC

- Employee disputes

It can be avoided:

- Start using payroll software with built-in statutory calculations

- Maintain templates for different scenarios

- Train your staff and your client’s payroll staff on statutory rules

- Double-check calculations before submission

Poor Record-Keeping

Payroll records are your safety net during audits. To keep your practice and client safe during the audit, you must invest in making them audit-ready.

What happens when you neglect record-keeping:

- Frequent scattered files

- Lack of centralised storage

- Inconsistent documentation

Impact:

- Difficulty during HMRC inspections

- Inability to prove compliance

- Delays in resolving disputes

How to avoid it:

- Store all payroll records digitally

- Maintain organised folders by client and payroll period

- Backup data securely (cloud storage preferred)

- Keep records for at least 3 years

Payroll Compliance Penalties: What Happens If You Get It Wrong?

Non-compliance with payroll regulations in the UK will lead to serious consequences, which are:

Late RTI submission → £100+ per incident

PAYE penalties

| Number of defaults in a tax year | Penalty percentage applied to the amount that is late in the relevant tax month (ignoring the first late payment in the tax year) |

| 1 to 3 | 1% |

| 4 to 6 | 2% |

| 7 to 9 | 3% |

| 10 or more | 4% |

How Technology Helps You Stay Payroll Compliant

Modern payroll software and cloud-based systems are transforming compliance:

Automation

- Automatically calculate PAYE, NI, and pensions

- Generate payslips and reports

- Reduce manual errors

Integration

- Connect payroll to accounting systems (Xero, QuickBooks, Sage)

- Sync employee and financial data

Alerts & Reminders

- Notify of upcoming deadlines

- Highlight discrepancies

And an even better idea is to combine it with outsourced payroll support like Equallto

Frequently Asked Questions About Payroll Compliance

What is a payroll compliance checklist?

It’s a list of steps to ensure your clients are adhering to UK tax laws, and pension regulations. The goal of following the checklist is to protect your clients and your practice from HMRC investigations and audits.

A payroll checklist will contain basic personal details, pay rate and hours worked, gross and net pay, deductions for income tax and National Insurance, and any pension contributions.

What are the main payroll compliance requirements in the UK?

a. PAYE and NI deductions

b.Statutory pay (SSP, SMP, etc.)

c. Pension contributions

d. Accurate reporting to HMRC via RTI

e. Record-keeping

How often should payroll compliance be reviewed?

a. Monthly audits recommended

b. Quarterly reviews for larger practices

c. Annual review at year-end

What are common payroll issues?

Some of the common payroll issues or errors are missing tax reporting, misclassifying employees and contractors, ignoring local laws, inaccurate record keeping, and errors in wage calculations. Not addressing these issues will lead to penalties, legal action, and loss of employee trust.

Conclusion

Payroll compliance is not just a regulatory requirement; it is a foundation for trust, accuracy, and growth in UK accounting practices.

- Accurate payroll protects employees, reduces fines, and enhances reputation.

- Structured processes and checklists reduce risk.

- Technology and automation save time, reduce errors, and improve efficiency.

Outsourcing to experienced partners like Equallto, we offer a perfect combination of payroll outsourcing services with technology that helps practices scale while maintaining compliance.

In 2026, success isn’t about processing payroll faster; it’s about processing it correctly, consistently, and confidently.