There is no P11D vs P11D(b); both are equally important in managing employee benefits and tax obligations. Both these forms contain taxable expenses and benefits provided to employees by their employers throughout the year.

To explain in a simple way:

- P11D form reports benefits and expenses given to an individual employee by the employer.

- P11D(b) form informs HMRC how much Class 1A National Insurance your client will need to pay for the benefits provided to their employees, and to declare that they have sent the forms to HMRC.

But we have noticed that many small accounting practices get confused with both of these forms, leading to missing deadlines and incomplete forms. Take, for instance, an accounting practice that was handling payroll for multiple SME clients. But for a whole year, they submitted just P11D forms of their employees to the HMRC, not the P11D(b). The consequence was that HMRC issued a penalty notice because the Class 1A NIC declaration was missing.

The issue was not a lack of effort but a breakdown in process visibility.

This is becoming increasingly common as compliance requirements grow more detailed and firms handle larger client volumes with leaner teams. But once you understand the differences between P11D and P11D(b), create structured workflows, and use the right systems, compliance becomes easier.

For that, we have created a guide that covers everything that you need to know about P11Ds and P11D(b), from deadlines and common mistakes to best practices, tools, and compliance strategies.

Understanding P11D and P11D(b) Forms

There is no need to do a P11D vs P11D(b) because both are related to employee benefits in kind and expenses, but they serve different purposes.

A P11D form is used for reporting taxable benefits and expenses given by your clients to their employees or directors during the tax year.

These benefits may include:

- Company cars

- Private medical insurance

- Interest-free loans

- Travel expenses

- Accommodation benefits

- Fuel benefits

- Gym memberships

- Non-payrolled benefits

Every employee who receives these benefits will require a separate P11D form, and it must be submitted to the HMRC, which will determine how much tax the employee owes on those benefits.

P11D(b) works differently; rather than reporting benefits of each employee, it summarises your client’s total liability for Class 1A National Insurance contributions on taxable benefits provided to employees.

The client employers use the P11D(b) to:

- Declare the total taxable benefit value

- Calculate Class 1A NIC owed

- Confirm whether benefits were provided during the year

Even if all benefits are payrolled, employers may still need to submit a P11D(b).

To cut a long story short:

- P11D contains the employee benefit details

- P11D(b) employer NIC declaration

Understanding this distinction is critical for accurate filing.

Who Needs to Submit P11D and P11D(b) Forms?

Many of your SME clients assume only large businesses are required to complete these forms, but that’s not true.

Businesses Required to Submit P11Ds

Employers must submit P11Ds when they provide taxable benefits or reimbursed expenses that are not processed through payroll.

This includes businesses offering:

- Company vehicles

- Health insurance

- Director benefits

- Travel reimbursements

- Beneficial loans

- Accommodation benefits

Businesses Required to Submit P11D(b)

A P11D(b) is required when your client employer:

- Has submitted P11Ds

- Provided taxable benefits

- Owes Class 1A NIC on employee benefits

Even if no tax is due, HMRC will expect a declaration confirming whether benefits were provided.

Important Deadline:

The P11D and P11D(b) forms must be submitted to the HMRC by 6 July after the end of the tax year.

The payments of Class 1A NIC are usually due by:

- 22 July if paying electronically

- 19 July if paying by post

Missing these deadlines can trigger automatic penalties for your clients of £100 per 50 employees for each month or part month your P11D(b) is late. Your clients will also be charged penalties and interest if there are delays in paying HM Revenue and Customs.

It is important to note that effective April 2027, HMRC is making the payrolling of most Benefits in Kind (BiKs) mandatory. Instead of calculating and submitting annual P11D and P11D(b) forms, employers will report and tax these perks (e.g., company cars, private medical) in real-time through regular payroll.)

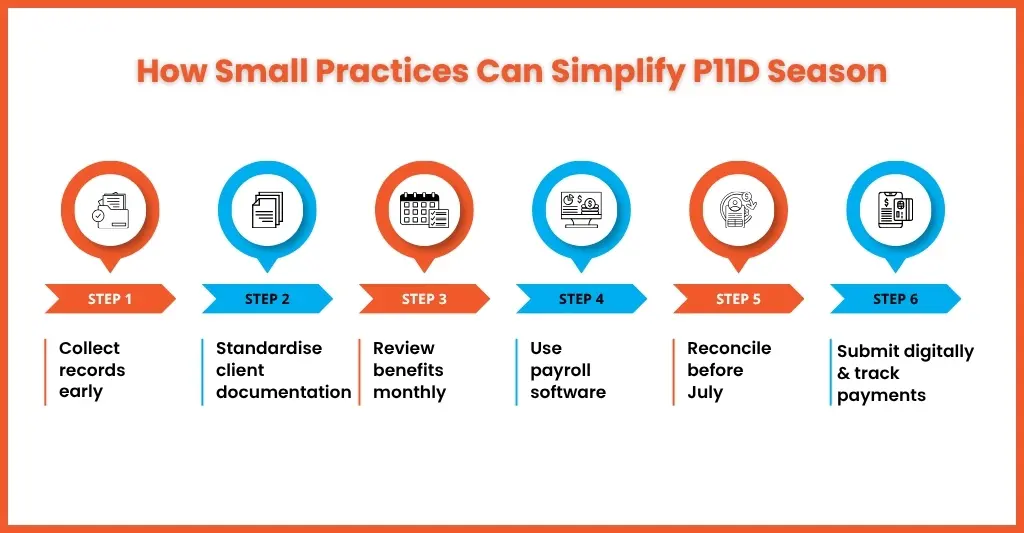

Step-by-Step Guide to Completing P11D Forms

To execute P11Ds accurately, you will require more than just numbers. You will need to follow the steps that will help you get clean records and organised workflows.

Step 1: Gather Employee Benefit Information

Begin with a collection of all the relevant data, which includes:

- Payroll records

- Company car details

- Insurance premiums

- Reimbursed expenses

- Director benefits

- Fuel usage records

Get all this information from your clients at the earliest to smooth the process.

Step 2: Verify Taxable Benefits

Not all employee expenses are taxable. Review HMRC guidance carefully to determine:

- Exempt expenses

- Taxable benefits

- Reimbursed costs

- Payrolled benefits

Misclassification is one of the major errors that keep occurring and must be avoided at all costs.

Step 3: Complete Individual Employee Forms

Start preparing P11Ds for each employee of your client who has received taxable benefits.

Make sure you correctly include:

- Employee details

- National insurance number

- Benefit descriptions

- Taxable values

- Dates and periods covered

Any mistake in this will have direct consequences for the employee tax calculations.

Step 4: Validate Figures

Before you submit, verify the following:

- Payroll records

- Accounting systems

- Expense claims

- Benefit schedules

Small discrepancies can create big compliance issues later, causing trouble for your client.

Step 5: Submit to HMRC and Employees

Once the P11Ds are verified and completed, you will need to send them to the HMRC and provide a copy of them to the employees. They will use this information to understand how benefits impact their tax position.

Step-by-Step Guide to Completing P11D(b) Forms

In P11D(b), the focus will be on your client’s employer liability rather than on employee taxation.

Step 1: Calculate Total Taxable Benefits

Calculate all the taxable benefits given to all employees and reported in the P11Ds. This will form the basis of the employer’s Class 1A NIC calculation.

Step 2: Calculate Class 1A NIC

You will need to calculate the amount of Class 1A National Insurance due on taxable benefits. The NIC rate will change annually, so keep an eye on the HMRC rates.

Step 3: Confirm Benefit Status

The P11D(b) also confirms whether:

- Benefits were provided

- Benefits were paid

- Class 1A NIC applies

This declaration is essential for HMRC compliance tracking.

Step 4: Submit the P11D(b)

Submit the completed P11D(b) digitally through HMRC-recognised software before the deadline. Late submission penalties can apply even when no NIC is owed.

Step 5: Pay Class 1A NIC

Once the submission is done, ensure payment is made to the HRMC correctly before the due date, 22 July online and 19 July if paying by cheque.

Common Mistakes When Filing P11D vs P11D(b) Forms

Instead focussing on P11D vs P11D(b), efforts must be made to avoid errors on P11Ds and P11D(b) forms that keep happening. This happens due to multiple reasons, like misunderstandings about taxable benefits, how to calculate their value, and so on. To reduce the risks of mistakes, we have listed the common errors:

Confusing Between P11D and P11D(b)

Many clients often make the mistake of doing P11D vs P11D(b) or thinking that P11Ds and P11D(b) are the same. But it’s not; both forms often need to be submitted together.

Missing Deadlines

P11D compliance deadlines come shortly after the end of the tax year, which is the time when you will be overloaded with work. Without structured workflows, submissions will get delayed. Without structured workflows, submissions can easily be delayed.

Incorrect Benefit Classification

Benefits are often:

- Incorrectly exempted

- Duplicated

- Undervalued

- Inconsistently reported

This creates potential HMRC scrutiny.

Inaccurate Class 1A NIC Calculations

Errors in NIC calculations will lead to underpayments or overpayments for your clients. Such situations create unnecessary administrative work later and reduce your practice’s reliability.

Incorrectly Valuing Benefits

Determining the ‘cash equivalent’ of certain benefits, such as company car usage, can be complex. Using HMRC’s approved methods and guidance is key to accurate valuation.

This is why practices are now focusing heavily on standardised documentation and digital workflows.

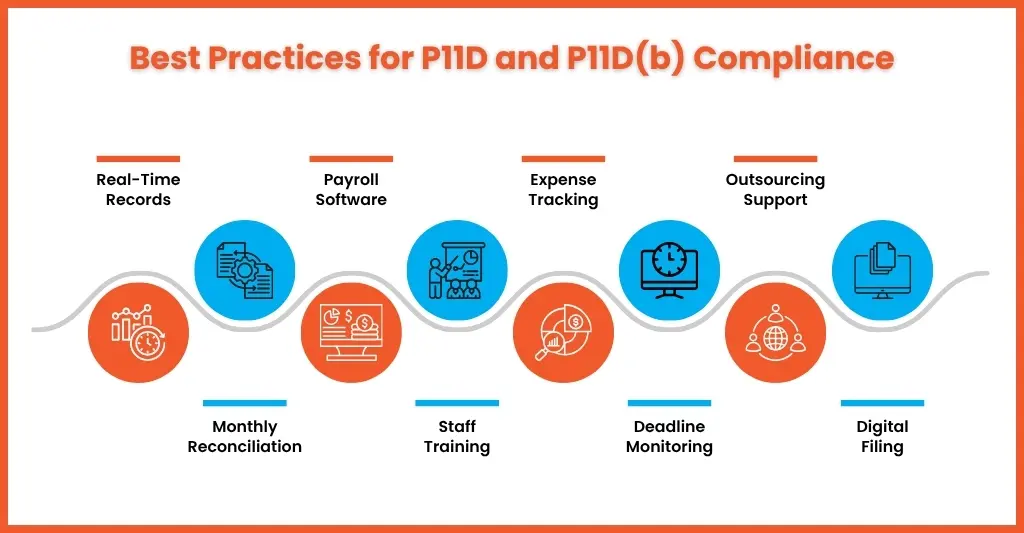

Best Practices for P11D and P11D(b) Compliance

To keep the P11Ds and P11D(b) accurate, forget about last-minute efforts and start working on a year-round process that makes your effort less taxing.

Here are some of the best practices you must follow:

Maintain Real-Time Records

Stop the practice of collecting data on benefits given to employees at the end of the year and make it a daily practice of collecting it. This will reduce errors, bringing in information in real-time and avoiding missing out on anything.

Standardise Benefit Tracking

There are certain workflows that are common across all businesses, such as:

- Company car records

- Expense reimbursements

- Healthcare benefits

- Payroll integration

Standardise them so that accuracy goes up significantly

Reconcile Monthly

Start the practice of monthly reviews to avoid year-end nasty surprises. Such monthly reviews will disclose:

- Duplicate entries

- Missing records

- Incorrect classifications

- Incomplete employee information

Identifying these errors beforehand instead of year-end will save you and your clients from a lot of hassle.

Train Staff Regularly

P11D rules keep changing at regular intervals. That’s why keep training and informing your team about it so that they understand:

- Reporting rules

- Exemptions

- Filing deadlines

- NIC obligations

Use Outsourced Support Strategically

The above-mentioned practices require additional investments in human resources, which small accounting practices cannot spare. That’s why many are choosing to outsource parts or entire payroll tasks to specialist providers like Equallto, offering renowned payroll outsourcing services.

Adopting outsourcing for payroll and bookkeeping is a solution that has multiple benefits will achieve many goals; you will be able to manage peak workloads, maintain compliance with HMRC regulations, and handle pressure well without the need for additional hiring of accountants.

Tools and Resources for Accurate P11D vs P11D(b) Filing

Wherever you require, take the help of technology to improve your filing accuracy and efficiency.

Payroll Software

Modern payroll software’s have become a main stay among accounting practices. Without using MTD-compliant accounting software you only dream of automating your P11D filing. Through it, you can automate:

- Benefit tracking

- Class 1A NIC calculations

- Reporting schedules

- Employee records

Some of the popular UK-compatible platforms include:

- Xero Payroll

- QuickBooks Payroll

- Sage Payroll

- BrightPay

Expense Management Systems

Along with accounting software, you must also use tools that enable accounting software to do that jobs even better like extracting data. These tools are:

- Dext

- Pleo

- Expensify

help maintain accurate expense documentation and digital audit trails.

HMRC Digital Services

HMRC, through various initiatives (MTD), is promoting digital filing and record-keeping among practices and clients. And as per HMRC directive, forms P11D and P11D(b) must be submitted online, and paper forms are no longer accepted by HMRC. These digital format records will reduce a considerable amount of paperwork and improve your client’s submission tracking.

Workflow Management Platforms

Firms handling multiple clients often benefit from workflow tools that track:

- Deadlines

- Approval stages

- Submission status

- Reconciliation reviews

This reduces the risk of missed filings.

FAQs About P11D vs P11D(b) Forms

What is the difference between a P11D and a P11D(b) form?

P11D form records the taxable benefits given to an individual employee by your client’s employer. A P11D(b) summarises the employer’s Class 1A National Insurance liability on those benefits.

There is one P11D form for each employee and a single P11D(b) to gather all the Class 1A National Insurance liabilities.

Who should fill out a P11D(b) form?

Employers who provide taxable employee benefits and owe Class 1A NIC generally need to complete a P11D(b).

Are there digital alternatives to filing P11D and P11D(b) forms?

These days, almost all practices or their outsourcing partner use HMRC and MTD-compliant accounting software to do digital filing and record keeping. This helps in being accurate, compliant as per MTD, and efficient.

How do I correct a mistake on a submitted P11D?

To correct a submitted P11D, you must inform HMRC about the mistake and provide the correct information. This can typically be achieved online via HMRC’s website or by sending a letter outlining the errors and corrections.

Are all employees required to receive a P11D?

No, not all employees are required to receive a P11D. It’s only necessary for those receiving benefits in kind, exceeding the HMRC’s set thresholds, that are not processed through payroll.

Conclusion

Stop with P11D vs P11D(b) and start getting mastery over both because they are absolutely crucial for your client employers to report taxable benefits in kind and comply with HMRC regulations accurately.

As HMRC compliance expectations increase, you will have to manage:

- Employee benefit reporting

- Class 1A NIC calculations

- Digital filing requirements

- Audit-ready documentation

With far greater precision than before.

With structured workflows, real-time record-keeping, digital tools, and the right operational support, you can reduce errors, avoid penalties, and manage year-end reporting far more efficiently.

These days, practices are placing their trust in outsourcing service providers that combine automation with expert support to manage their growing workloads and compliance needs without overloading their internal teams. That’s where Equallto comes in as a saviour for small accounting practices, ensuring their reporting remains accurate, scalable, and manageable during busy seasons.

Stay informed, meet deadlines, and seek professional guidance by contacting us. We will streamline the entire P11D process for you.