James runs a small accounting practice in Kent, and on the 15th, he gets an email from a client in his inbox.

“Hi James, just checking, have we already paid this invoice?”

Suddenly, he realised that the invoice was overdue by 32 days, and now, instead of focusing on advisory calls, he was digging through email threads to confirm balances.

Is this your story, too?

Multiple studies point out that late payments cost UK small businesses billions annually and affect cash flow stability. Meanwhile, the Federation of Small Businesses (FSB) reports that over 50,000 UK SMEs close each year due to cash flow pressures, many due to unpaid invoices, making statement of accounts important.

A properly designed statement of account becomes more than a document; it becomes a control tool.

What Is a Statement of Account?

Statement of account, also known as accounts statement and customer statement, contains all the transactions (invoices, payments, and outstanding balances) between your client and its customer within a specific period. Statement of account helps in:

- Calculating outstanding account balance

- Reminding customers to settle their account balance

- Avoid disputes with customers

No wonder your clients keep asking for a statement of account so that they can remind their customers to pay their overdue invoices.

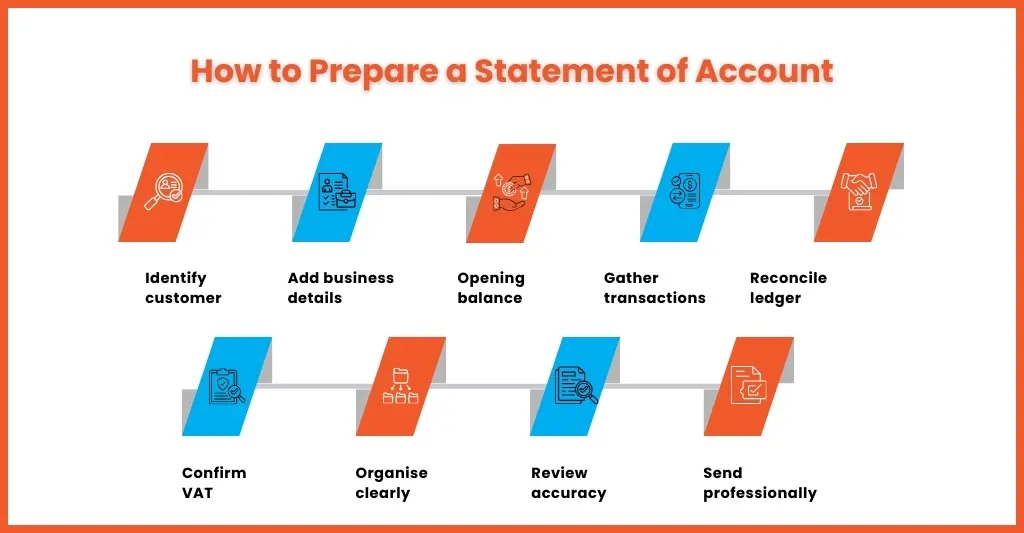

How to Prepare a Statement of Account

A statement of account contains the summary of all invoices, payments, and outstanding balances within a specific period, thus helping in resolving disputes and improving cash flow.

The following steps will help you prepare a professional statement of account.

Step 1: Identify the Customer and Period

Start the process by identifying your client’s customer to whom this statement will be sent. Enter its name, contact details, and account number. Set the statement period to clearly specify which transactions are included.

Step 2: Add Your Business Details

Add your clients’ business name, logo, address, and contact details at the top of the statement. This will give it a professional look and ensure the customer knows where this document is coming from.

Step 3: List Opening Balance

If the customer has an outstanding balance from previous periods, record it as the opening balance. This helps track the total due amount from the start of the statement period.

Step 4: Gather All Transaction Data

Start pulling out all the information related to your client from your accounting system. The data to be extracted are:

- All invoices (including partially paid)

- All payments received (including bank transfers and card payments)

- Credit notes and refunds

- Any journals affecting receivables (e.g., reclassifications)

Step 5: Reconcile the Ledger

Performing this step will save you from embarrassment later.

Do these quick checks first:

- Bank reconciliation is up to date (especially for client payments)

- Your A/R (Debtors) control account aligns with the customer ledger total

- Payment references match invoices where possible

- Old items (90+ days) have notes or reasons (“query”, “client raised dispute”, “awaiting PO”)

Payments often land in the bank without clear references. If they aren’t allocated properly, your statement will show invoices as unpaid, even when the client has paid.

Step 6: Confirm VAT Treatment

Under HMRC MTD VAT rules, invoices must show VAT correctly where applicable, and the statement must show the same.

Confirm the following:

- Correct VAT rates used (standard / reduced / zero / exempt / outside scope)

- Credit notes reflect VAT consistently

- VAT inclusive/exclusive totals match what was invoiced

- No VAT-coded entries are sitting in suspense

Present the VAT on the statement as follows:

- Show invoice totals including VAT (most common for clients)

- Or show net + VAT breakdown (useful for commercial clients who reconcile input VAT)

Step 7: Organise Chronologically to Make it Client-Friendly

A strong statement of account is one that your client and its customers can understand easily. It will include the following:

- Opening balance (what was outstanding before this statement period)

- Each invoice (date, reference, amount)

- Each payment received (date, amount, reference)

- Any credit notes or adjustments

- Closing balance (total due)

Format the statement of account using clear columns such as Date, Reference, Description, Debit, Credit, and Balance. Group it by month if the statement period is long, and highlight overdue amounts separately.

Step 8: Review and Verify Accuracy

Double-check all entries to ensure no transaction is missing or duplicated. Accuracy is critical for maintaining trust and preventing disputes.

Step 9: Send or Share the Statement

Once finalised, send the statement of account to the customer via email or through your accounting system.

These steps you can execute in two ways; in-house or outsourcing accounting. choice is yours.

Why a Statement of Account Is Critical for UK Practices?

There are several benefits that make the statement of account very critical for UK practices. These benefits include:

Encourages Prompt Payments

A well-made statement of accounts will contain clear statements detailing balances, due dates, and services, leading to faster payments.

Facilitates Easier Reconciliation

A clear and detailed statement will help your client’s customers to reconcile charges with their records, thus reducing disputes.

Reduced Queries

A detailed statement of account provides information on services, costs, and payment status, answering client questions beforehand, thus reducing calls and emails from them.

Enhances Credibility and Trust

A professional statement of account will showcase your attention to detail and clear communication, supporting transparency between your practice and your client, thus enhancing your credibility among your clients.

Statement of Account vs Invoice – Key Differences for UK Firms

An invoice is a request for payment for a specific transaction, while a statement of account provides a comprehensive overview of all the transactions that have taken place during a set period. A statement of account contains invoices, payments received, and outstanding balances.

Let’s understand the difference in a better way.

| Invoice | Statement of Account |

| Requests payment for one transaction | Summarises multiple transactions |

| Sent when service is provided | Sent periodically (e.g., monthly) |

| Contains VAT breakdown | Shows overall outstanding balance |

| Single due date | Consolidated payment overview |

An invoice asks for money, and a statement of account reminds your clients what they owe in total. Both are important but serve different purposes.

Statement of Account Example for UK Accounting Firms

Let’s look at a simplified statement of account example:

Client: ABC Accounting Ltd

Period: 1 January – 31 March 2026

| Date | Description | Debit (£) | Credit (£) | Balance (£) |

| 01/01 | Opening Balance | 0 | – | 0 |

| 05/01 | Invoice #101 | 1,200 | – | 1,200 |

| 18/01 | Payment Received | – | 1,200 | 0 |

| 02/02 | Invoice #108 | 950 | – | 950 |

| 01/03 | Invoice #115 | 600 | – | 1,550 |

Closing Balance: £1,550 due

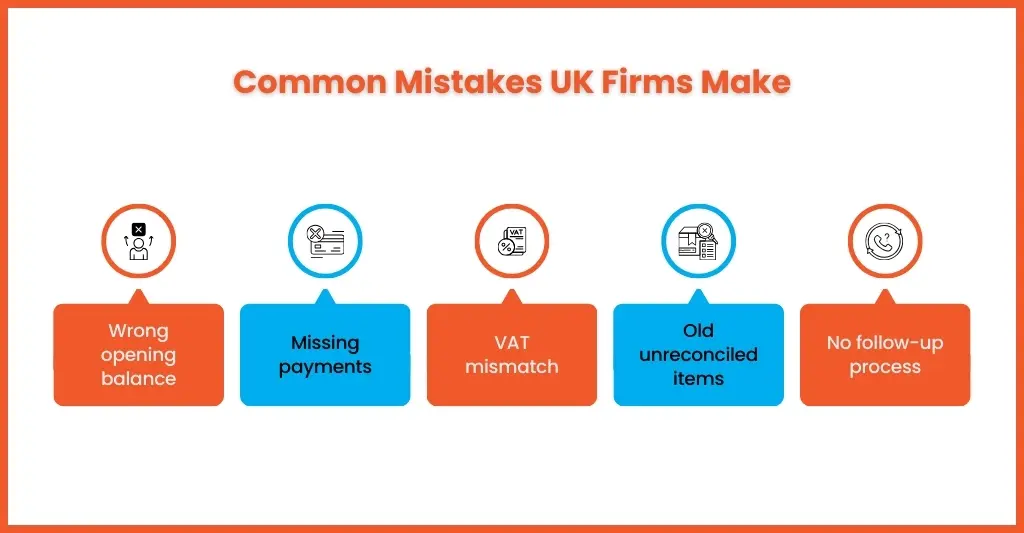

Common Errors UK Practices Make in Statements of Account

Errors do happen while making statements of accounts, some rarely and some quite commonly, and it’s the common ones which you must be careful of because of their potential consequences.

Here are some common pitfalls:

- Incorrect opening balance, which will lead to client disputes and mistrust.

- Missing transactions or payments will complicate reconciliation.

- Unclear descriptions or invoice references create doubt, which will confuse your clients and lead to delayed payments.

- Outdated client contact information

- Vague payment terms or missing payment details

- Sending to the wrong client will breach confidentiality and damage your reputation.

- Not following up on overdue statements leads to poor cash flow.

These common errors must be avoided at all costs, and if you require outside assistance in this endeavour, you can use the year-end outsourcing services offered by experienced accounting outsourcing services, which is the future of accounting.

People Also Ask

What is included in a statement of account for UK clients?

Ideally a statement of account should include the following:

Opening balance

Invoices

Payments

Credit notes

Closing balance

VAT details (where applicable)

How does a statement of account help with HMRC compliance?

It ensures accurate VAT tracking, reconciled balances, and clear audit trails, supporting compliance under HMRC record-keeping rules.

Can Xero or QuickBooks generate a statement of account automatically?

Yes. Both platforms allow automated statement generation. However, accuracy depends on clean bookkeeping and reconciled ledgers.

What is a statement of account in the UK?

It is basically a snapshot or summary of the transactions that are executed between the seller and the customer.

Who needs a statement of account?

Your clients need statement of account to keep track on outstanding payments from their customers. It helps them to remind their customers to pay their overdue invoices.

Conclusion

Remember James from Kent, he followed the same structured monthly statement of accounts and a clear follow-up process. The results were something changed.

- Fewer payment queries

- Faster collections

- Less stress

A statement of account, when used properly, can become an effective tool to control cash flow. For small accounting practices, the statement of account is not administrative paperwork. It’s leverage.

At Equallto, we expand on that leverage with structured bookkeeping, accounts receivable management, and financial process support, helping you maintain accuracy, improve client communication, and strengthen cash control without increasing internal pressure.

Need assistance with the statement of accounts? Connect with us and see the difference.