Are you stuck between bookkeeping vs accounting and what’s different between them? Here’s what you need to know: bookkeeping records the numbers, and accounting interprets those numbers.

That’s the core difference.

But for UK accounting practices in 2026, the real question isn’t just what is bookkeeping vs accounting, it’s how do you structure both efficiently without overwhelming your team?

Let’s understand this better with an example.

A small accounting practice in the UK was expanding fast. It was acquiring new clients, but the team was stuck with:

- Data entry

- Reconciliations

- Document chasing

When the month-end came, there was no time left for:

- Financial analysis

- Tax planning

- Advisory work

There was no dearth in expertise; it was the confusion around the difference between bookkeeper and accountant roles and how to balance them. It’s a challenge faced by many, especially small accounting practices with limited resources.

The result?

- Overworked teams

- Delayed reporting

- Missed growth opportunities

To avoid such a situation for your practice, we have prepared this guide where we’ll break down:

- What bookkeeping vs accounting really means

- What makes a bookkeeper different from accountant?

- When you need each role

- How technology is changing both

- And how to structure your practice for efficiency

What Is Bookkeeping vs Accounting? A Clear, Simple Definition

Let’s first answer the core question.

What is bookkeeping vs accounting?

Bookkeeping is the process of day-to-day recording and organising of financial transactions.

It includes:

- Recording sales and expenses

- Reconciling bank accounts

- Maintaining financial records

- Organising invoices and receipts

Accounting involves analysing, interpreting, and reporting on financial data collected during the bookkeeping to provide strategic insights.

It involves:

- Analysing financial data

- Preparing financial statements

- Tax planning and compliance

- Advising on business decisions

Difference Between Bookkeeper and Accountant

At first glance a bookkeeper and accountant look same but dive a little deeper and you will see the difference. Without them, doing bookkeeping and accounting is difficult and that makes understand the difference between them important.

| Feature | Bookkeeper | Accountant |

| Role | Records transactions | Analyses and interprets data |

| Focus | Day-to-day financial data | Financial insights and compliance |

| Skills | Data entry, reconciliation | Tax, reporting, advisory |

| Output | Clean financial records | Financial reports and strategy |

| Timing | Ongoing | Periodic (monthly, quarterly, yearly) |

A bookkeeper will keep the data accurate, and an accountant will ensure something useful comes out from that data.

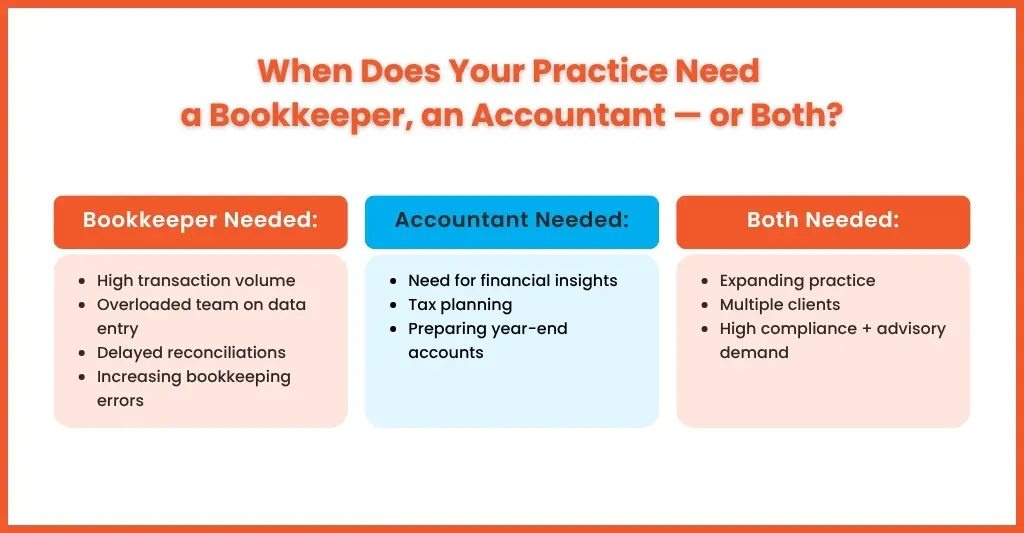

When Does Your Practice Need a Bookkeeper, an Accountant — or Both?

This is where the majority of the accounting practices hit a roadblock, not because of the confusion in understanding bookkeeping vs accounting, but in understanding its roles.

Here’s when you need to hire a bookkeeper:

You Have to Deal with High Transaction Volumes

If your clients generate:

- Daily sales transactions

- Multiple bank entries

- Frequent expenses

Then, bookkeeping becomes time-intensive very quickly. Without a bookkeeper you will end up spending hours keeping up with it.

Your Team Spends Too Much Time on Data Entry

If your accountants are bogged down with:

- Posting transactions

- Categorising expenses

- Uploading invoices

That’s a red flag. These are low-value tasks that don’t require high-level expertise.

Reconciliations are Delayed

When bank reconciliations are not updated in real-time:

- Reports become unreliable

- VAT submissions become stressful

- Errors start compounding

It’s a sign that your bookkeeping capacity is insufficient.

Bookkeeping Errors are Increasing

Are getting errors repeatedly, such as:

- Duplicate entries

- Incorrect categorisation

- Missing transactions

It’s the sign of poor bookkeeping, which will lead to poor accounting outcomes.

When You Need an Accountant:

Once your books are clean, you will have to make sense of the numbers generated, and that’s where accountants come in. Here are some signs that you need an accountant:

You Need Financial Insights

If your clients are frequently asking questions like:

- “Why is profit declining?”

- “Where are we losing money?”

- “How can we improve margins?”

You need to answer that, and without an accountant, you cannot give the right answer. Bookkeeping only gives you precise numbers; accounting gives you accurate answers.

You’re Planning Tax Strategies

Tax planning requires:

- Deep understanding of regulations

- Forecasting

- Strategic decisions

It is not a bookkeeper’s cup of tea; it requires accounting expertise.

Preparing Year-End Accounts

While preparing year-end accounts of your clients, you will need to work on:

- Adjustments

- Accruals

- Compliance checks

- Financial statements

Doing it effectively requires professional accounting knowledge, which only an accountant or a third party accountant possesses.

When You Need Both

Most professional accounting practices need to handle both:

- Multiple clients

- When practice is expanding

- Demand for compliance and advisory services increases

Ideally, you need both.

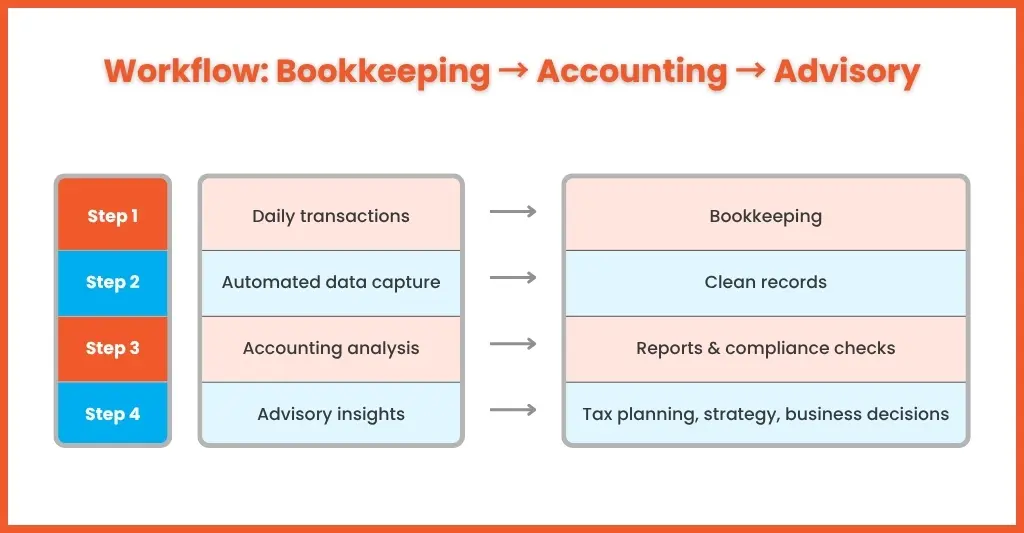

How Technology and AI Are Changing Both Roles for UK Practices

Technology is no longer in a supporting role for accounting practices; it is reshaping the entire bookkeeping vs accounting model. Due to HMRC’s MTD initiative and its expansion, accounting work is moving from manual processing → automated systems → human insight, and AI tools, MTD-VAT compliant accounting software, and data-grabbing tools are aiding practices in achieving that.

But adopting a tool or software does not do the trick; there should be a change in processes.

Automation in Bookkeeping (From Data Entry to Data Flow)

Bookkeeping used to be:

- Manual data entry

- Spreadsheet-based tracking

- End-of-month updates

But with the introduction of cloud and automation tools, things have changed completely.

These modern tools now handle:

- Bank feeds: Transactions flow automatically into systems like Xero and QuickBooks

- Transaction categorisation: Rules and AI suggest correct categories

- Invoice capture: Tools like Dext and Hubdoc extract data from receipts and invoices

- Real-time syncing: Data updates instantly across systems

It means your practice will no longer have to endure:

- Backlog at month-end

- Manual errors

- Get faster turnaround times

Continuous bookkeeping instead of reactive bookkeeping

Bookkeeping is no longer about entering data.

It’s about:

- Reviewing automated entries

- Managing exceptions

- Ensuring data accuracy

AI in Accounting

Accounting is also evolving, and AI in accounting is having the biggest impact.

AI tools are now helping with:

- Financial analysis: For identifying trends and performance issues

- Forecasting: For predicting cash flow and future outcomes

- Anomaly detection: Flagging unusual transactions or errors

- Automated reporting: Generating insights instantly

A new study by Xero in partnership with Cebr (Centre for Economics & Business Research) and Censuswide shows that extensive AI implementation has yielded productivity gains for 46% of UK accountants and bookkeepers. Meaning AI is deciding the future of accounting.

What does it mean for your practice?

- Less time spent on calculations

- More time spent on interpretation

- Increased focus on advisory services

Can One Person Do Both Bookkeeping and Accounting?

Theoretically, one person can handle both bookkeeping and accounting, but practically, it’s difficult.

One person can handle both only if your practice has a:

- Small client base

- Low transaction volume

- Simple business structures

But it becomes a problem when:

- Client volume becomes high

- Complex compliance requirements come up

- Tight deadlines

Risks of combining roles:

- Team burnout

- Rise in errors

- Delayed reporting

- Reduction in advisory capacity

A smart approach will be to separate roles or explore outsourcing a part of the workload. After detailed analysis of in-house accounting and outsourcing, many practices have successfully divided the workload among their:

- In-house accountants

- Outsourced bookkeeping support

The result of outsourcing bookkeeping and accounting has shown better efficiency without increasing labour costs.

Frequently Asked Questions: Bookkeeping vs Accounting

Is bookkeeping the same as accounting?

Many think that bookkeeping and accounting are the same, but they’re not. Bookkeeping is the process of day-to-day recording and organising of financial transactions. Accounting involves analysing, interpreting, and reporting on financial data collected during the bookkeeping to provide strategic insights.

Which is more cost-effective for a small UK practice — a bookkeeper or an accountant?

Most small accounting practices are into routine accounting tasks that can be managed effectively by a bookkeeper. When they jump into giving advisory services and compliance-related work, accountants are better suited.

What does Making Tax Digital mean for bookkeeping and accounting?

With the introduction and expansion of the MTD initiative by HMRC, a few tasks have been added while doing bookkeeping and accounting.

a. Digital record-keeping while doing bookkeeping

b. Regular submissions and compliance while doing accounting

This increases the importance of both roles.

Is AI replacing bookkeepers?

AI will not replace those bookkeepers who use it for automating routine, repetitive tasks like data entry, receipt scanning, and categorisation. Using AI, bookkeepers can shift from manual processing to high-value advisory services.

What can an accountant do that a bookkeeper cannot?

A bookkeeper can handle basic financial recordkeeping and simple reporting, but they usually can’t provide strategic financial analysis, tax planning, or complex business advice that accountants offer.

Final Verdict: What Does Your UK Practice Really Need?

It’s time for you to stop debating on bookkeeping vs accounting. Bookkeeping is the input, and accounting is the output + strategy; both are important and required for building an efficient practice.

If your bookkeeping is weak:

- Your reports will be inaccurate

- Your compliance risk increases

If your accounting is weak:

- Your business decisions suffer

- Growth slows down

For your practice to succeed, you will need to have:

- Strong bookkeeping foundation

- Skilled accounting oversight

- Efficient workflows

- Scalable support

Here’s where the solutions of Equallto can make a difference. By supporting bookkeeping processes, Equallto helps practices:

- Reduce workload

- Improve accuracy

- Manage multiple clients efficiently

- Free up time for advisory services

Don’t choose between bookkeeping and accounting; choose us by filling out our contact form and get the benefit of both, which will help your practice grow.